Articles

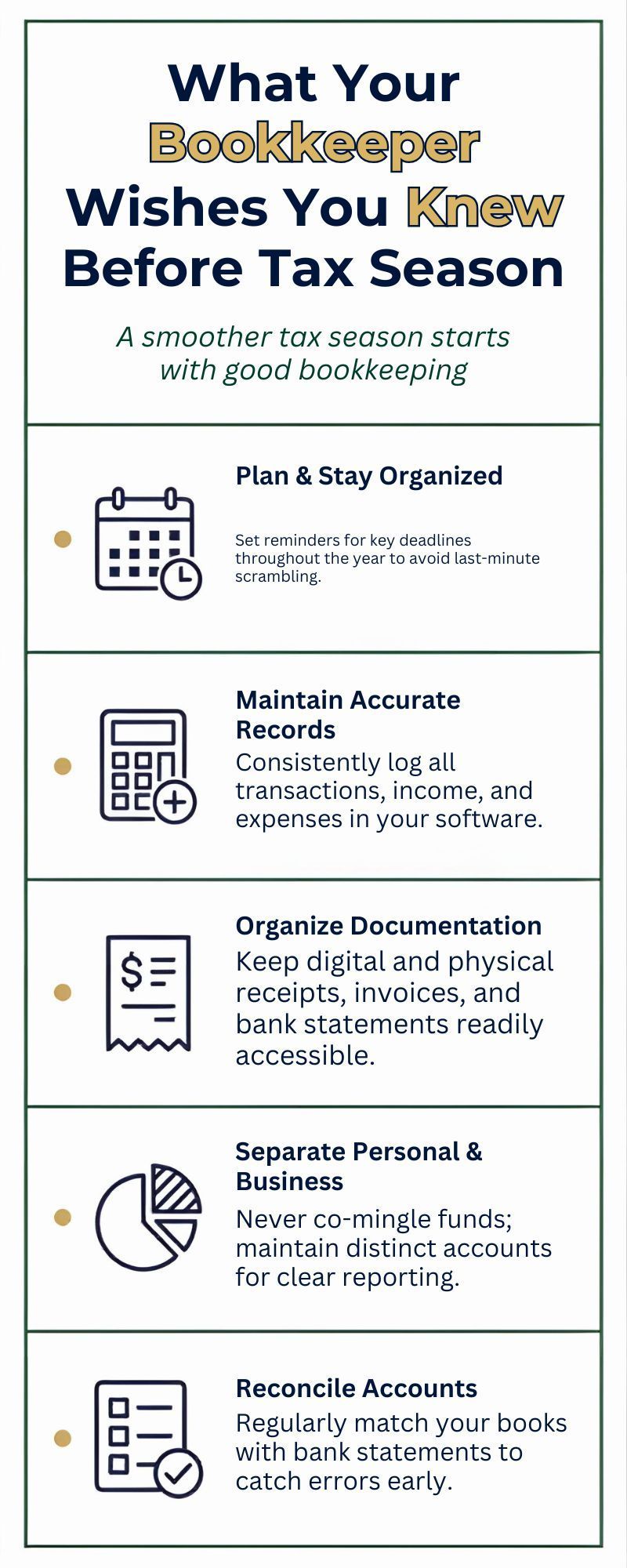

For many small business owners, tax season feels stressful, confusing, and rushed. Documents are being gathered at the last minute, questions pop up unexpectedly, and everyone is trying to meet deadlines. But the truth is, tax season doesn’t have to feel that way. A lot of the stress that happens in March and April could be avoided with better bookkeeping habits throughout the year. As bookkeepers, we see the same patterns every year, and there are a few things we wish every business owner understood before tax season arrives.

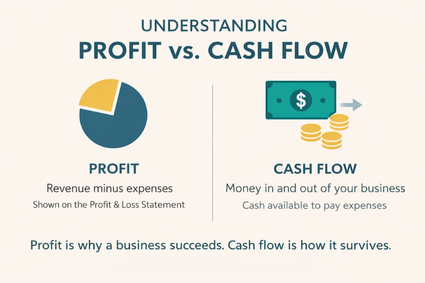

Many small business owners assume that if their company is profitable, they must be financially healthy. Unfortunately, that’s not always true. One of the most common financial misunderstandings is confusing profit with cash flow . While they are connected, they are not the same—and understanding the difference can protect your business from serious financial stress.

A new year is the perfect time for small business owners to reset, refocus, and build better financial habits. While motivation is high in January, the businesses that truly succeed are the ones that rely on systems and routines—not guesswork —to manage their finances. Strong bookkeeping habits create clarity, reduce stress, and support smarter decision-making all year long. Here are the essential financial habits every small business should establish to start the year strong.

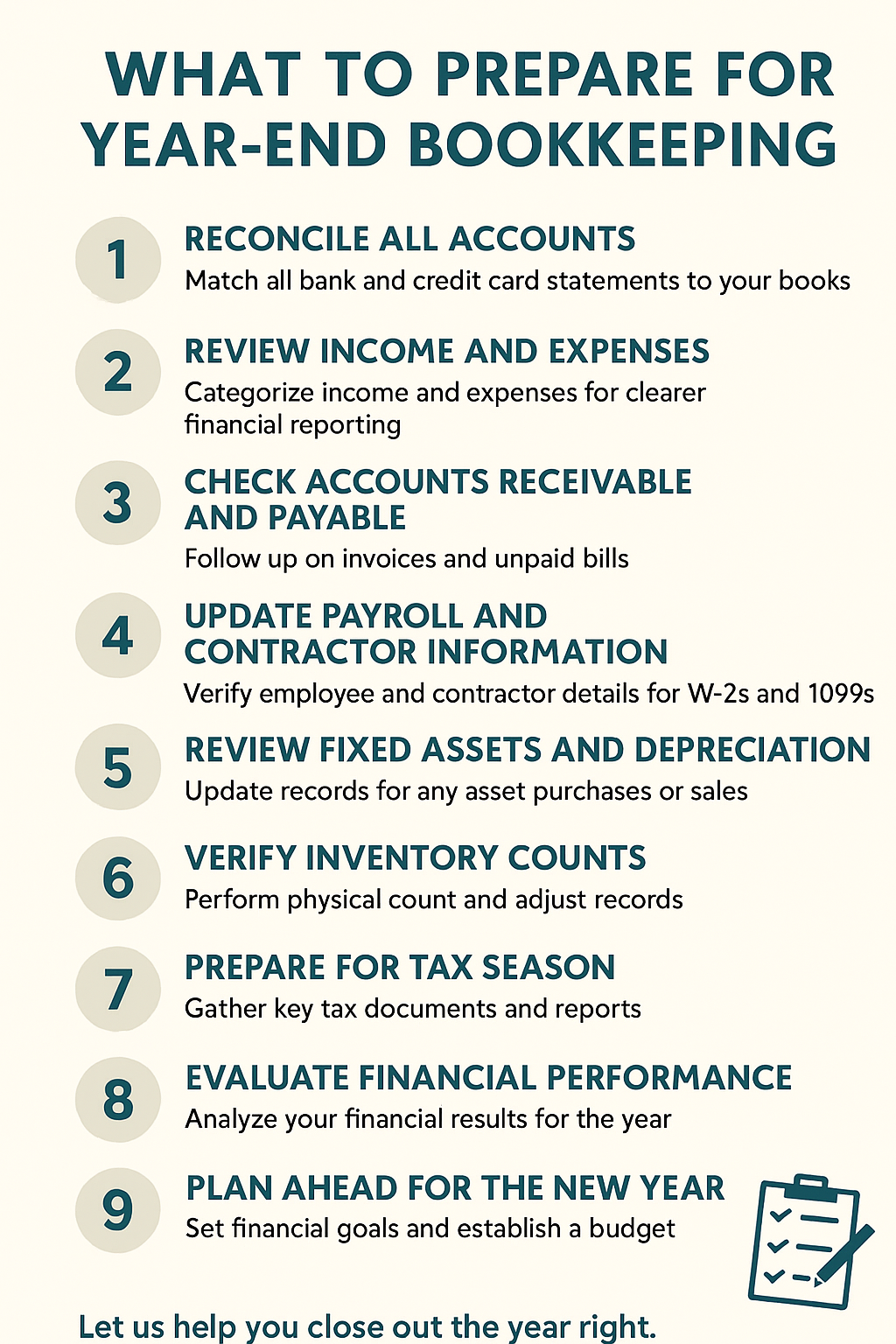

A new year brings new goals, new opportunities, and a fresh chance to move your business forward with confidence. But before you can set smart financial goals for the year ahead, you need a clear picture of where you’ve been—and that’s where bookkeeping plays a vital role. Accurate bookkeeping gives you the financial visibility needed to make informed decisions. Here’s how wrapping up the year properly sets you up for success:

A Practical Guide for Small Business Owners

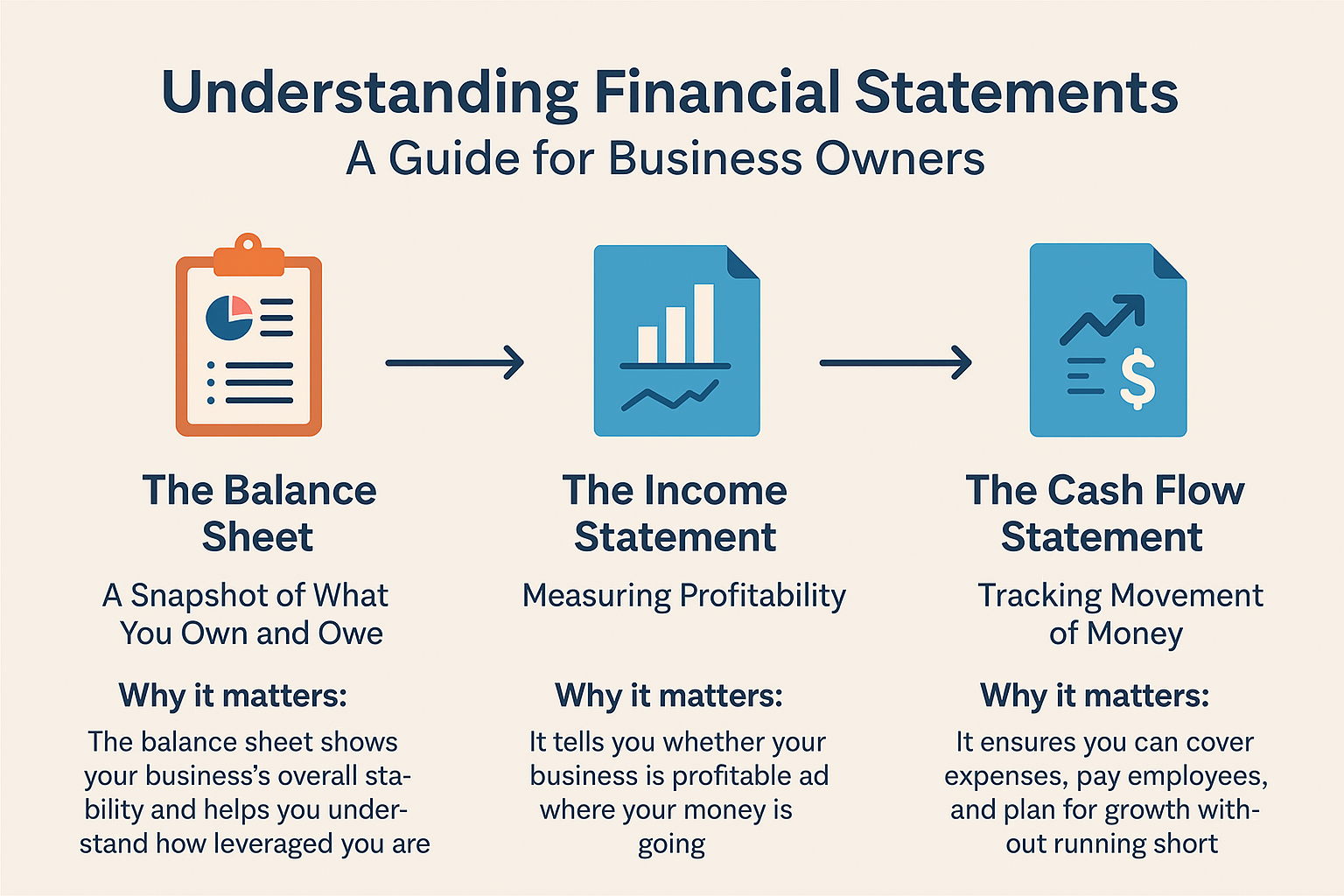

A Guide for Business Owners Financial statements are the roadmap to your business’s financial health. Yet many small business owners see them as a mystery—numbers, charts, and terms that feel more confusing than helpful. The truth is, once you understand what these statements are telling you, they become powerful tools for making better business decisions. At LOV Bookkeeping, we help clients go beyond just “having the books done.” We make sure they understand what their numbers mean. Here’s a simple breakdown of the three key financial statements every business owner should know.

In today’s digital world, small businesses rely heavily on technology to manage finances. While this makes bookkeeping faster and more efficient, it also means sensitive financial data is more vulnerable than ever. A data breach or security lapse can lead to financial loss, compliance issues, and damage to your reputation. At LOV Bookkeeping, we understand how important it is to protect your information. Here are some best practices to keep your financial data safe and secure.

When it comes to managing your business finances, there’s no one-size-fits-all approach. Every business has unique goals, challenges, and workflows — which means your bookkeeping should be just as unique. Custom bookkeeping goes beyond simply “keeping the books” — it aligns your financial tracking and reporting with your specific business needs, helping you make smarter decisions, save time, and set the stage for growth.

Bookkeeping is one of those behind-the-scenes tasks that can either support your business’s success or quietly undermine it. At LOV Bookkeeping, we’ve seen firsthand how small missteps in managing financial records can lead to major headaches. The good news? Most of these mistakes are entirely avoidable. Here are the top five bookkeeping mistakes small businesses make—and how to steer clear of them.

How bookkeeping supports better financial planning and decision-making